In today’s technological climate, manually balancing your checkbook with pen (or pencil) and your register likely has gone the way of the dodo bird.

But, knowing exactly what comes out and goes into your checking account not only is one of the best ways to combat fraud, it can give you a true idea of where your money is going and of your spending habits.

Most of your transactions and account information likely is readily available to you anytime in both your banking app and when you access your online banking account. You may even have a budgeting app linked to help you keep track of your expenses. So it may seem pointless or even redundant to keep track and balance your expenditures.

But with so many transactions these days, it’s easy to forget about one that hasn’t cleared your account yet. So if you regularly log all of your transactions, you always will know exactly how much money truly is in your account – to the exact cent.

And best of all, it doesn’t take long to learn, but it will require diligence on your part.

First, you should determine your account’s balance. Try to avoid using your debit card and writing checks for a couple of days to avoid any transaction-clearing lag. After waiting a few days, log into your banking app or online banking account to check your balance. Cross-reference the balance displayed against any automatic withdraws or outstanding checks. For instance, if your balance is $850.67, but you wrote a check to pay a water bill for $49.47, ensure that check has cleared. Otherwise, you’ll need to subtract the $49.47 from the $850.67 displayed balance.

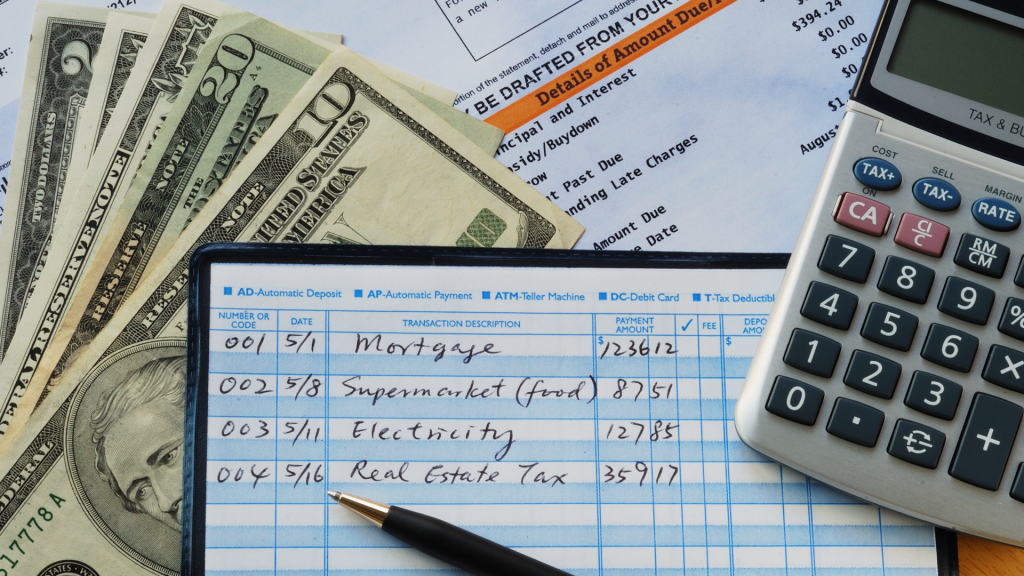

Once you have determined your true balance, now, it’s just a matter of simple math. Just update your balance in your checkbook register by keeping track of each withdrawal and deposit as they occur. This includes debit card transactions as well as checks and automatic payments, as well as your payroll deposits if you have direct deposit.

Once you start logging each transaction, you can cross-reference to what posts to your account. You can either wait until you receive your monthly statement, or you can check daily or every other day, denoting each transaction in your ledger that clears and ensuring the totals match.

By keeping a running total of your transactions, your balance should match the balance on the statement. If the balances don’t match, check your register to see if a transaction has not been processed, if the bank has a record of a transaction that you do not have recorded in your register (then check this transaction to ensure it’s one you recognize or simply forgot to log) or if the amount of one of the transactions differs from what you registered.

If the balances still do not match, check your register and receipts against the record from the bank. Also check for any mathematical mistakes in your register (math mistakes happen to all of us!). If you believe an error has occurred, contact your bank.

Despite checkbooks and checks becoming more obscure in today’s technological landscape, having a handle and knowing just how much money is in your account always will be the most important tool you can have in your financial toolbox and is key to your financial health.

Tracking your transactions keeps you keenly aware of just how much money you have, helps you detect problems and, most importantly, allows you to plan ahead financially.

Financially Fit is your home fitness guide for all things financial, provided by RCB Bank. Find money-building tips, insights and inspiration to help you improve your financial well-being at RCBbank.com/GetFit. Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. Member FDIC.