DO NOT GIVE OUT YOUR INFORMATION! We will never contact you asking for your Online Banking username and password, debit card number or your PIN.

Cryptocurrency, or “crypto,” has surged in popularity, with digital currencies like Bitcoin gaining widespread use. However, this popularity has also made it a target for scammers, leading to consumers losing over $1 billion to crypto scams in the first half of 2022, as reported by the Federal Trade Commission (FTC).

The appeal of crypto for scammers lies in its decentralized nature, the irreversible nature of transactions and the general lack of understanding among most people about how crypto operates. The absence of a centralized authority to flag suspicious transactions makes it an attractive playground for fraudsters.

Scammers employ various methods to initiate contact with potential victims, such as email phishing, SMS text messages (smishing), phone calls, packages and social media. They often use personal information to target victims or even imitate someone known to the victim. One common tactic is to promise unrealistically high returns on crypto investments.

The process involves instructing victims to convert US dollars into Bitcoin and send it to a specific digital address, frequently using Bitcoin ATMs for the transaction. Once the funds are transferred, the irreversible nature of crypto transactions leaves victims with no recourse.

To avoid falling victim to crypto scams, consumers are advised to exercise caution when dealing with cryptocurrency transactions. Running transactions through professionals like banks, CPAs or tax professionals can help verify legitimacy. Additionally, individuals should not send money on behalf of others and extra scrutiny is needed for checks received via non-USPS mail services.

If a situation seems suspicious, consulting trusted advisors is crucial. Scammers often employ tactics like repeated contact, harassment and pressure to prevent victims from seeking advice or reporting the situation to authorities.

In case you have already fallen victim to a scam, steps can be taken to mitigate further harm. Victims should contact the FBI through ic3.gov to report identity theft, reach out to the bank’s fraud department, and remain vigilant against future scam attempts.

Overall, the rise in crypto popularity has brought about a parallel surge in scams, making it imperative for consumers to educate themselves, exercise caution and seek professional advice before engaging in cryptocurrency transactions.

As winter approaches and holiday travel plans take center stage, winter wanderers must be on high alert for potential scams lurking in various forms. From deceptive emails to cunning calls and enticing social media posts, scammers are ramping up their efforts to exploit the joyous spirit of the season. Here’s how to navigate the winter wonderland of travel without falling prey to fraud.

Social Media

Social media, a hub for festive cheer, is also a breeding ground for travel scams. Criminals imitate well-known hotels and resorts online, but their sites include misleading information, such as fake hyperlinks and phone numbers. Eager holiday-goers may find themselves making payments for dream getaways that exist only in the virtual realm leaving them empty-handed and out of pocket.

Robocalls

Robocalls, often associated with automated holiday greetings, can also mask sinister intentions. If your phone rings with an automated message, especially regarding travel, the safest bet is to hang up promptly. Legitimate travel agencies steer clear of robocalls, making them a clear red flag for potential scams.

Allow your winter travel experiences to be filled with pleasure and amazement, rather of the traps of frauds. Stay vigilant, stay informed, and ensure your winter holidays are as magical as they should be.

Booking Sites Before booking winter travel offers, diligent research on the company is essential. While reviews and ratings provide insights, individual needs differ. Beware of seemingly irresistible deals, such as complimentary airline tickets, as scammers use these as bait to hook unsuspecting victims.

Cancellation Policies

Protect your winter escapades by always securing a receipt and understanding cancellation policies before confirming any reservations. Having these policies in writing serves as a crucial record should disputes arise later.

Wi-Fi Connections

As snow blankets landscapes, scammers attempt to cover their tracks with fraudulent schemes. Regularly monitor your financial accounts for any suspicious activity. Embrace the convenience of online banking but do your best to steer clear of public Wi-Fi networks that could compromise your security. Because they are vulnerable, public Wi-Fi networks present a serious threat. Visit RCB Bank Online Banking Tools here.

Planning a winter getaway? Alert your bank in advance. Provide details about your destinations and travel dates to ensure smooth financial transactions without unexpected disruptions.

Should the unfortunate happen and you find yourself entangled in a travel scam, swift action is imperative. Contact our RCB Bank support team at 1.855.226.5722 on weekdays between 8:00 a.m. and 6:00 p.m. CST. For weekend assistance, dial 1.877.361.0814 on Saturdays from 8:00 a.m. to 4:00 p.m. and Sundays from 8:00 a.m. to 12:00 p.m. (excluding Federal Holidays). Additionally, contribute to combating fraud by filing a complaint with the FBI at ic3.gov.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Aspiring homeowners are no strangers to the challenges of securing mortgage approval, and in this quest, one often-overlooked factor emerges as a crucial element —the elusive credit score.

In the world of real estate, where dreams of owning a home come with a price tag, understanding the connection between credit scores and mortgage approval rates can be a game-changer. Your credit score is not only a number representation; it has the ability to significantly impact your ability to get a mortgage and become a homeowner.

Your credit score is more than just a score—it’s a passport to your homeownership journey. There is a direct link between higher credit scores and the likelihood of having that mortgage application stamped with approval.

The industry has long acknowledged credit scores as an essential metric of financial trustworthiness. Yet, what many may not realize is the extent to which lenders rely on this three-digit number to gauge an individual’s financial habits and risk potential.

Digging into the intricacies, it becomes apparent that a higher credit score not only secures better interest rates but significantly boosts the odds of getting that coveted nod from lenders. In a landscape where competition for mortgage approvals is fierce, understanding the nuances of credit scores becomes a strategic advantage.

What does this mean for the average home seeker? It’s a call to action, urging individuals to be proactive in cultivating a credit profile that appeals to lenders. Timely bill payments, debt reduction, and vigilant credit report monitoring are highlighted as key steps in this journey towards creditworthiness.

Schedule an appointment with an RCB Bank Mortgage representative today for more information while you search for your dream home. You can also take advantage of RCB Bank’s Loan Promotion to Save $500 by December 31, 2023. Click Save500 today!

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. Offer available for most purchases and refinances. With approved credit on RCB Bank Mortgage secondary market loans locked between October 1, 2023 and December 31, 2023. Must meet minimum loan and program underwriting requirements. Lender credit must be used toward borrower closing costs. Not redeemable for cash or down payment funds. This offer is not valid with any other RCB Bank Mortgage incentives, promotions or discounts. OHFA Bond and 5/5 ARM products are not eligible for promotional credit. This offer is subject to change or terminate without notice. Other loan terms and restrictions apply. RCB Bank is an Equal Housing Lender. NMLS #798151 and Member FDIC

As the real estate market continues to evolve, prospective homebuyers are faced with various choices and decisions. One of the pivotal considerations in the homebuying process is understanding the distinction between Mortgage Pre-Approval and Pre-Qualification. To shed light on this often-confusing subject, experts weigh in to help homebuyers make informed decisions.

Mortgage pre-approval and pre-qualification are frequently used interchangeably, but they carry different implications and serve distinct purposes in the home financing journey. According to financial experts, the differences lie in how thoroughly each process is evaluated.

Mortgage Pre-Qualification

Mortgage pre-qualification is the preliminary step in the home loan process. It involves a basic assessment of an individual’s financial situation based on self-reported income, debts, and credit. Lenders use this data to provide a rough estimate of the loan amount a borrower might be eligible for. It’s a valuable starting point for those beginning their homebuying journey, offering a snapshot of their financial capacity.

Mortgage Pre-Approval

On the other hand, mortgage pre-approval is a more comprehensive and rigorous process. It requires potential homebuyers to submit detailed financial documentation, including income verification, credit history, and other relevant information. The lender then conducts a thorough analysis to determine the exact loan amount a buyer qualifies for. A pre-approval holds more weight in the eyes of sellers, as it signifies a buyer’s seriousness and financial capability. Experts emphasize the importance of obtaining a mortgage pre-approval before house hunting in today’s competitive real estate market. Pre-approval simplifies the homebuying process and gives buyers an edge in a seller’s market.

While both pre-qualification and pre-approval have their place in the home financing process, understanding the key differences empowers buyers to make informed decisions aligned with their unique circumstances. As the real estate landscape evolves, education remains a powerful tool for aspiring homeowners navigating the path to homeownership.

Schedule an appointment with an RCB Bank Mortgage representative today for more information while you search for your dream home. You can also take advantage of RCB Bank’s Loan Promotion to Save $500 by December 31, 2023. Click Save500 today!

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. Offer available for most purchases and refinances. With approved credit on RCB Bank Mortgage secondary market loans locked between October 1, 2023 and December 31, 2023. Must meet minimum loan and program underwriting requirements. Lender credit must be used toward borrower closing costs. Not redeemable for cash or down payment funds. This offer is not valid with any other RCB Bank Mortgage incentives, promotions or discounts. OHFA Bond and 5/5 ARM products are not eligible for promotional credit. This offer is subject to change or terminate without notice. Other loan terms and restrictions apply. RCB Bank is an Equal Housing Lender. NMLS #798151 and Member FDIC

As we conclude October’s Cybersecurity Month, it is essential to reinforce the importance of safeguarding both yourself and your financial institution, such as RCB Bank, against the ever-present threat of phone-based social engineering. This form of cybercrime preys on trust and human vulnerability, making it crucial for individuals and institutions to stay vigilant.

Here are some final tips to keep in mind:

Verify Identities: When receiving phone calls requesting sensitive information, always take the time to verify the caller’s identity. Do not be hasty in sharing personal or financial details. To ensure that you are speaking with a legitimate representative, consider calling back using official contact details that you obtained independently from trusted sources.

Educate Yourself and Others: Knowledge is a powerful weapon against social engineering. Stay informed about common tactics employed by cybercriminals who aim to deceive you over the phone. Share this knowledge with friends and family to create a network of individuals who are equally vigilant. Protecting your circle can go a long way in thwarting potential threats.

Enable Multi-Factor Authentication (MFA): One of the most effective ways to enhance the security of your personal accounts is by enabling Multi-Factor Authentication (MFA). MFA adds an extra layer of protection by requiring more than just a password for access. Whenever possible, activate MFA on your accounts to make it significantly harder for cybercriminals to breach them.

Exercise Caution Online: Be cautious about sharing personal information on social media or other online platforms. Cyber attackers often exploit the information they collect from platforms such as Facebook, Instagram, LinkedIn, and others to craft convincing schemes. Protect your personal data online to make it more challenging for malicious individuals to target you.

Report Suspicious Calls: If you ever receive a suspicious phone call related to your RCB Bank account(s), it is imperative to report it promptly to RCB Bank. You can reach us at 855.226.5722. Timely reporting of such incidents can help the bank take action to protect your accounts and investigate potential threats.

Phone-based social engineering is a persistent threat that preys on trust and human vulnerability. By understanding the tactics used by attackers and remaining vigilant, you can protect both yourself and your financial institutions. Remember that skepticism is a valuable defense, and it is essential to prioritize your security over convenience when dealing with phone calls from unknown or suspicious sources. Cybersecurity is a shared responsibility and staying informed and cautious is key to defending against these threats.

Cybersecurity is a shared responsibility. By staying informed, you can enhance your digital defenses and protect yourself from the evolving landscape of cyber threats. Remember, vigilance is your greatest asset in the battle for digital security.

If you feel or think you detect fraud or are a victim of fraud call us at 855.226.5722 or visit our website RCBBank.Bank and click on Security Center for a variety of methods to keep you and your money safe and to stay up to date.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Our phones have evolved beyond mere communication devices, transforming into powerful tools for social engineering. Phone-based social engineering is a sophisticated threat that manipulates individuals into revealing confidential information or engaging in actions that compromise security. Recognizing the warning signs of these deceptive tactics is crucial to safeguard your personal and financial information.

Unsolicited Calls: One of the primary red flags is receiving unsolicited calls, especially from unknown numbers. These calls often involve requests for sensitive information or demands for immediate action. Scammers count on the element of surprise and pressure, making it essential to approach such calls with caution. Always verify the caller’s identity before sharing sensitive data or complying with their demands.

Urgency and Fear Tactics: Scammers are adept at creating a sense of urgency or fear, which puts their victims on the defensive. They aim to coerce individuals into making hasty decisions by inducing panic or stress. In these situations, taking a moment to pause and assess the call’s legitimacy is paramount. Legitimate organizations don’t resort to fear tactics to obtain your information.

Caller ID Spoofing: Another technique cybercriminals use is caller ID spoofing. Attackers can manipulate caller IDs to make it seem like they are calling from a trusted source, such as a bank or government agency. As such, never rely solely on caller ID information to determine the authenticity of a call. Always ask questions and verify the caller’s credentials independently.

Information Verification: Beware of callers who ask for personal or financial information over the phone, even if they claim to represent a legitimate organization. Legitimate institutions will typically offer alternative means of communication or verification. Only disclose your information over the phone if you know the caller’s identity.

Inconsistencies: Inconsistencies within the call, such as contradictory information or a caller who avoids answering direct questions, are often clear indicators of a scam. If something feels off during the conversation, trust your instincts. Cybercriminals rely on confusion and misdirection to achieve their goals.

Cybersecurity is a shared responsibility. By staying informed, you can enhance your digital defenses and protect yourself from the evolving landscape of cyber threats. Remember, vigilance is your greatest asset in the battle for digital security.

If you feel or think you detect fraud or are a victim of fraud call us at 877.361.0814 or visit our website RCBBank.Bank and click on Security Center for a variety of methods to keep you and your money safe and to stay up to date.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

In the digital age, deception has evolved into an artform, and phone-based social engineering has emerged as one of its most cunning creations. Deceptive tactics employed by these attackers often involve the impersonation of trusted entities or individuals to gain the trust of their unsuspecting victims. Let’s take a deeper dive into the intricate web of deception that these cybercriminals create.

Phishing Calls: Scammers are masters at deception who frequently disguise themselves as legitimate institutions such as banks or government agencies. Armed with a persuasive tone and a knack for manipulation, they call individuals with the intention of extracting sensitive information like Social Security numbers and credit card details. These calls, seemingly benign at first, can lead to disastrous consequences, with personal finances hanging in the balance. Phishing – What is it?

Vishing (Voice Phishing): Vishing is the darker, vocal sibling of phishing. Criminals employ a range of tactics in this malicious endeavor. They might deploy pre-recorded messages that demand immediate action or pose as authoritative figures like IT support or even law enforcement. The intention is to confuse individuals into revealing personal information or coercing them into transferring their hard-earned money into the pockets of these unscrupulous characters.

Pretexting: For attackers, crafting convincing backstories or pretexts is second nature. Impersonating a coworker in need of information for a supposed work-related task, these criminals exploit human empathy and trust. The victims, never suspecting the deceit, end up divulging sensitive data that can be exploited to the attacker’s advantage.

Impersonation: Some of these fraudsters take their deception to the next level, going to great lengths to mimic voices, mannerisms, and emotional tones. They may pose as a distressed family member or a colleague urgently seeking assistance. These emotionally charged calls prey on the victim’s sense of responsibility and sympathy, leading them down a treacherous path of deception.

Spear Phishing: In targeted attacks, these cybercriminals invest time in researching their victims. Armed with an extensive dossier, they craft highly personalized messages or calls. These communications reference specific events, acquaintances or people in the victim’s life, making them appear incredibly legitimate. This personalized touch elevates the deception to an entirely new level.

The world of phone-based social engineering is fraught with danger, where trust is leveraged as a weapon and deception reigns supreme. It’s imperative for individuals to remain cautious and verify the authenticity of callers before divulging any sensitive information, for the art of deception knows no bounds in the digital realm. A Word of Caution About Fraud

Cybersecurity is a shared responsibility. By staying informed, you can enhance your digital defenses and protect yourself from the evolving landscape of cyber threats. Remember, vigilance is your greatest asset in the battle for digital security.

If you feel or think you detect fraud or are a victim of fraud call us at 877.361.0814 or visit our website RCBBank.Bank and click on Security Center for a variety of methods to keep you and your money safe and to stay up to date.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

In today’s digital age, the term “cybersecurity” has become synonymous with safeguarding our digital lives. It’s the shield that guards our critical systems and sensitive information from the relentless onslaught of digital threats. Cybersecurity is the practice of protecting critical systems and sensitive information from digital attacks. These attacks can take many forms, ranging from identity theft to sophisticated scams. Understanding these threats is the first step in fortifying your digital fortress.

One of the most horrendous forms of cyberattacks is identity theft. This occurs when someone wrongfully obtains and uses your personal information, often for financial gain. Criminals may make unauthorized credit card transactions, apply for loans in your name and social security number or commit other fraudulent activities. To shield yourself from these threats, consider the following precautions:

Be vigilant: Never share personal information with unknown callers, texters, or email Verify the legitimacy of any organization before disclosing sensitive data.

Strong passwords: Avoid easily guessable passwords, such as family names or pet names. Opt for complex combinations of letters, numbers, and symbols. Refrain from writing down or storing passwords electronically, as lost devices could compromise your security.

Social media caution: Beware of oversharing on social media, as personal information gleaned from your profiles can be used against you. Visit: Online Quizzes

Regular credit checks: Obtain your free annual credit report to ensure its accuracy and detect any suspicious activities early.

Scams come in various disguises, from romance and gift card scams to fake home repair offers and even imposters posing as trusted institutions like your bank. Here’s how you can avoid falling prey to scams:

Verify charitable events: When approached with requests for donations or assistance related to disasters, always seek more information and ensure the legitimacy of the cause.

If it sounds too good to be true: Apply the age-old adage. If an offer seems suspiciously generous or unrealistic, it probably is.

Beware of contingencies: Never accept funds or sweepstakes winnings that require you to send money back. Legitimate winnings and gifts do not come with such conditions.

Cybersecurity is a shared responsibility. By staying informed and following these guidelines, you can enhance your digital defenses and protect yourself from the evolving landscape of cyber threats. Remember, vigilance is your greatest asset in the battle for digital security.

Visit our Security Center for a variety of methods to keep you and your money safe and to stay up to date.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Sources: Delesline, N., & Carlton, G. (2022, June 2). What, exactly, is cybersecurity? and why does it matter?. ZDNET. https://www.zdnet.com/education/computers-tech/what-is-cybersecurity-and-why-cybersecurity-matters/

The phone has become more than just a communication tool; it has become a powerful instrument for social engineering. Social engineering via phone involves manipulating individuals into revealing confidential information or performing actions that compromise their security.

The Art of Deception

Phone-based social engineering relies heavily on deception. Attackers often impersonate trusted entities or individuals to gain their target’s trust. Here are some common tactics they employ:

Phishing Calls: Scammers often pose as legitimate organizations, such as banks or government agencies, and call individuals to extract sensitive information like Social Security numbers or credit card details.

Vishing (Voice Phishing): Vishing involves manipulating victims through voice calls. Criminals may use pre-recorded messages or impersonate authority figures, like IT support or law enforcement, to trick individuals into revealing personal information or transferring money.

Pretexting: Attackers create convincing backstories or pretexts to manipulate victims into disclosing information. For instance, they might pose as a coworker seeking information for a work-related task.

Impersonation: Some attackers go to great lengths to mimic the voices and mannerisms of others. They may impersonate a family member in distress or a colleague in urgent need of assistance.

Spear Phishing: In targeted attacks, criminals research their victims to craft personalized messages or calls. These calls may reference specific events or people in the victim’s life, making them appear more legitimate.

Recognizing the Red Flags

Protecting yourself from phone-based social engineering begins with recognizing the warning signs:

Unsolicited Calls: Be cautious of calls from unknown numbers, especially if they request sensitive information or demand immediate action.

Urgency and FearTactics: Scammers often create a sense of urgency or fear to pressure victims into complying. Always take a moment to verify the caller’s identity.

Caller ID Spoofing: Attackers can manipulate caller IDs to appear as if they are calling from a trusted source. Never rely solely on caller ID information.

Information Verification: Be wary of callers who ask for personal or financial information over the phone, even if they claim to represent a legitimate organization.

Inconsistencies: If something about the call feels off, such as inconsistent information or a caller who avoids answering questions directly, it may be a red flag.

Protecting Yourself and The Bank

To safeguard against phone-based social engineering:

Verify Identities: Always verify the caller’s identity before sharing sensitive information. Call back using official contact details obtained independently to ensure you’re speaking with a legitimate person.

Educate Yourself: Stay informed about common social engineering tactics and be vigilant. Share this knowledge with friends and family to protect them as well.

Enable Multi-Factor Authentication (MFA): Whenever possible, enable MFA on your personal accounts to add an extra layer of security.

Use Caution Online: Be cautious about sharing personal information on social media or other online platforms, as attackers may use this information against you. Be aware that attackers utilize information they gather from FaceBook, Instagram, LinkedIn, and other social media platforms.

Report Suspicious Calls: If you receive a suspicious call for your RCB Bank account(s), report it to RCB Bank’s Fraud Department immediately. (1)877.361.0814

Phone-based social engineering is a potent threat that preys on trust and human vulnerability. By understanding the tactics used by attackers and remaining vigilant, you can protect yourself. Remember that skepticism is a valuable defense, and always prioritize your security over convenience when dealing with phone calls from unknown sources.

For more information on fraud and scams please visit our Security Center to stay up to date.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Sources: Risukhin, A. (2023, May 9). Social Engineering: What it is and how to protect yourself. ClearVPN. https://clearvpn.com/blog/what-is-social-engineering/

Refinancing your mortgage can be a tempting option for homeowners looking to lower their monthly payments or take advantage of lower interest rates. However, like any financial decision, there are pros and cons to consider before making the leap.

One of the biggest advantages of refinancing your mortgage is the potential to save money. If you can secure a lower interest rate than what you currently have, you could significantly reduce your monthly mortgage payments. This can free up extra cash that can be used for other expenses or savings. Additionally, refinancing can also allow you to switch from an adjustable-rate mortgage to a fixed-rate mortgage, providing stability and predictability in your monthly payments.

Another benefit of refinancing is the opportunity to tap into your home’s equity. If you’ve built up equity over time, refinancing can allow you to access that money for home improvements, debt consolidation, or other financial needs. This can be especially useful if you have high-interest debt that you want to consolidate into a lower-interest mortgage.

On the flip side, there are also some drawbacks to consider when refinancing your mortgage. One of the main cons is the cost associated with refinancing. Closing costs, appraisal fees, and other expenses can add up, making refinancing a costly endeavor. It’s important to carefully calculate whether the potential savings outweigh the upfront costs.

Another potential downside is the extended loan term that often comes with refinancing. While this can lower your monthly payments, it also means that you’ll be paying off your mortgage for a longer period of time. This can result in paying more interest over the life of the loan, even if you secure a lower interest rate.

Lastly, refinancing may not be an option for everyone. Lenders typically require a certain credit score and income level to qualify for refinancing. If your financial situation has changed since you initially obtained your mortgage, you may not meet the necessary criteria to refinance.

To summarize, refinancing your mortgage can offer significant benefits such as lower monthly payments, access to home equity, and financial flexibility. However, it’s important to carefully weigh the potential savings against the upfront costs and extended loan terms. Additionally, not everyone may qualify for refinancing, so it’s crucial to assess your financial situation and consult with a mortgage professional before making a decision.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. With approved credit. For specific questions regarding your personal lending needs, please call RCB Bank at 855-BANK-RCB. Some restrictions apply. RCB Bank is an Equal Housing Lender, NMLS #798151 and Member FDIC.

In today’s digital age, technology has become an integral part of our lives, revolutionizing the way we work, communicate and even manage our finances. From mobile banking apps to budgeting tools and investment platforms, technology offers a plethora of opportunities to enhance our financial well-being.

Embrace Mobile Banking

Gone are the days of standing in long queues at the bank. RCB Bank mobile banking has made it incredibly convenient to manage your finances on the go. With just a few taps on your smartphone, you can check your account balance, transfer funds (RCB Bank’s OneWayPay, Bank to Bank Transfers), pay bills and even deposit checks. It not only saves time but also allows you to keep a close eye on your transactions, ensuring better financial control and security.

Harness the Power of Budgeting Apps

Budgeting is a crucial aspect of financial fitness and technology has made it easier than ever. Along with RCB Bank’s myCardswap, and other numerous budgeting apps, such as Mint and YNAB (You Need a Budget), are available to help you track your expenses, set savings goals, and monitor your progress. These apps provide visual representations of your spending habits, offer personalized insights, and send alerts to help you stay within your budget. By using these tools, you can make smarter financial decisions and achieve your financial goals faster.

Automate Your Savings

Saving money consistently can be challenging, especially when it requires manual effort. However, technology has introduced automated savings tools that make the process effortless. Automatic transfers to savings with RCB Bank’s myClickSwitch as well as apps such as Mint and YNAB analyze your spending patterns. By leveraging this technology, you can effortlessly build an emergency fund, build investment and save for long-term goals without even realizing it.

Explore Investment Platforms

Investing was once considered a complex and intimidating task, but technology has democratized the investment landscape. Online investment platforms offer easy access to various investment options, including stocks, bonds, mutual funds, and exchange-traded funds (ETFs). With user-friendly interfaces, educational resources, and automated portfolio management, these platforms have made investing more accessible and transparent, empowering individuals to grow their wealth.

Leverage Online Marketplaces

If you have unused items lying around, technology has made it effortless to declutter and make some extra money. Online marketplaces such as eBay, Amazon, and Facebook Marketplace provide platforms for selling used goods. You can easily create listings, reach a wide audience, and receive payments securely. By selling items you no longer need, you not only declutter your living space but also generate additional income.

Utilize Comparison Websites

Whether you’re looking for insurance or credit cards technology has simplified the process of comparing various financial products and services.

In an era defined by technological advancements, it is crucial to embrace the tools and platforms available to enhance our financial fitness. By leveraging mobile banking, budgeting apps, automated savings tools, investment platforms, online marketplaces and comparison websites, we can optimize our financial management, save time, increase our savings and make smarter financial decisions. However, it’s important to remember that while technology can be a powerful ally in achieving financial fitness, it should be used responsibly. Stay vigilant about online security, keep your personal information secure, always research and verify the credibility of the apps and platforms you choose to use.

Dive in and harness the power of technology to gain better control over your finances. By doing so, you’ll be well on your way to achieving your financial goals and securing a brighter future.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Sources:

FinanceBuzz. (2023, May 4). Best budgeting apps [2023]. FinanceBuzz. https://financebuzz.com/budgeting-apps

Tepper, T. (2023, July 5). 5 best investment apps of July 2023. Forbes. https://www.forbes.com/advisor/investing/best-investment-apps/

In the journey toward financial fitness, it’s important to recognize that everyone makes mistakes. We’ve all had our share of financial ups and downs, and dwelling on past financial problems can hinder our progress. The key to achieving true financial well-being lies in embracing a ‘forgive and forget’ mindset. By learning from our past mistakes and letting go of any lingering guilt or regret, we open the door to a brighter future. In this article, we explore the transformative power of ‘forgive and forget’ when it comes to our personal finances.

Embrace Forgiveness

Forgiving yourself for past financial missteps is crucial for your mental and emotional well-being. Self-sabotaging thoughts about your financial past will prevent you from moving forward. Accept that mistakes happen and understand that they are opportunities for growth. Embrace the mindset that forgiveness is not about excusing your actions but about releasing yourself from the burdens of guilt and shame.

Remember that you are not alone in experiencing financial challenges. Many successful individuals have faced similar struggles and managed to bounce back. Oprah Winfrey, one of the world’s most influential women, encountered numerous financial setbacks in her early career but persevered and achieved remarkable success. Learn from these stories and realize that forgiveness paves the way for a fresh start.

Learn from Your Mistakes

While it’s important to forgive, learning from your past financial mistakes is equally crucial. Take the time to reflect on what went wrong and identify the factors that contributed to your financial difficulties. By understanding the root causes, you can develop strategies to avoid repeating those same mistakes in the future.

Consider seeking financial education and guidance to enhance your knowledge and skills. Learn about budgeting, investing and other essential financial concepts. The more you educate yourself, the better equipped you’ll be to make informed decisions and mitigate future financial risks.

Letting Go of Regret

Forgiving yourself also means letting go of regret. Regretting past financial decisions only consumes your energy and prevents you from moving forward. Instead, focus on the present moment and the steps you can take to improve your financial situation. Create a realistic plan to address your current financial goals and commit to it with determination and discipline.

Developing a positive mindset is essential in your financial journey. Surround yourself with supportive individuals who believe in your ability to achieve financial success. Engage in activities that bring you joy and reinforce your sense of self-worth. By cultivating a positive outlook, you’ll be better equipped to face future challenges and make sound financial choices.

Create a Fresh Financial Narrative

Forgiveness and forgetting your past financial problems allow you to create a fresh narrative for yourself. Rather than defining yourself by past mistakes, focus on the future and the potential for growth and success. Visualize your desired financial future, set clear goals and take actionable steps to achieve them.

Remember that building financial fitness takes time. Stay committed and celebrate each small victory along the way. By cultivating resilience and determination, you’ll be well on your way to financial well-being.

In the quest for financial fitness, forgiving yourself and forgetting your past financial problems are essential steps toward creating a brighter future. Embrace forgiveness, learn from your mistakes and let go of regret. By doing so, you will develop a positive mindset and create a new narrative that focuses on growth, resilience and success. Remember, your past does not define you. Your ability to forgive and move forward will shape your financial well-being and lead you toward a prosperous future.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Online quizzes sure seem like innocent fun. But before you take that next personality test, quick survey or “find out what type of BLANK you are” quiz, ask yourself: Do I know who’s gathering this information about me – and what do they plan to do with it?

The more information you share on these quizzes, the more you risk that information being misused, the Federal Trade Commission stated earlier this month.

A lot of the times, these quizzes and/or surveys will ask questions similar to the questions that are asked on online account security. Scammers can post a seemingly innocent quiz, then use your quiz answers to try and reset your online accounts, letting them steal your bank and other account information, the FTC warns.

One major way to protect your personal information — in addition to maintaining strong passwords and using multi-factor authentication — is to steer clear of online quizzes … or just don’t answer them truthfully, the FTC advises.

Another type of online quiz to be on the lookout for are quizzes that offer prizes for completion.

These quizzes may look official, giving gift cards as prizes to some of your favorite online establishments. And once you finish the quiz, you’ll be sent to a page where you are to enter your personal information so that the scammers can send you or award you your prize.

Once they have your personal information, coupled with some of the answers that were provided on the quiz, scammers can wreak havoc before you even know what happened.

If you suspect that an online quiz is a phishing scam, tell a friend. Then, report it to the FTC at ReportFraud.ftc.gov.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

It’s almost the new year, which means it’s time for new year’s resolutions. According to a survey by Statista, financial goals are one of the top 5 areas where Americans wish to focus on improving.

If improving your finances is an area in which you’d like to focus, here are some ways in which that could be obtained.

Start a financial journal. If you keep track of every penny you spend, you may see things on paper that you don’t notice day to day. Keeping a journal will make you more mindful of where your money goes.

Starting a journal will help you if you want to organize your finances. Organizing your finances can reduce stress by showing you where you stand financially and can help you start a path to financial success.

Reduce your debt. Paying down your debt always is a good place to start with a new year’s resolution. Your debt-to-income ratio plays an important part in your finances, so finding a strategy to eliminate your debt can be a great boost to your financial well-being.

Improve your credit score.Improving your credit score can make it easier for you to get approved for loans and lines of credit, and even lower interest rates. A person with a higher credit score can save thousands of dollars over the course of their life than someone with a low score.

Making financial resolutions can help you make 2023 the best ever and even more enjoyable beyond that. Whether you want to reduce debt or save money, you can build financial security by setting these types of resolutions.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

In today’s technological climate, manually balancing your checkbook with pen (or pencil) and your register likely has gone the way of the dodo bird.

But, knowing exactly what comes out and goes into your checking account not only is one of the best ways to combat fraud, it can give you a true idea of where your money is going and of your spending habits.

Most of your transactions and account information likely is readily available to you anytime in both your banking app and when you access your online banking account. You may even have a budgeting app linked to help you keep track of your expenses. So it may seem pointless or even redundant to keep track and balance your expenditures.

But with so many transactions these days, it’s easy to forget about one that hasn’t cleared your account yet. So if you regularly log all of your transactions, you always will know exactly how much money truly is in your account – to the exact cent.

And best of all, it doesn’t take long to learn, but it will require diligence on your part.

First, you should determine your account’s balance. Try to avoid using your debit card and writing checks for a couple of days to avoid any transaction-clearing lag. After waiting a few days, log into your banking app or online banking account to check your balance. Cross-reference the balance displayed against any automatic withdraws or outstanding checks. For instance, if your balance is $850.67, but you wrote a check to pay a water bill for $49.47, ensure that check has cleared. Otherwise, you’ll need to subtract the $49.47 from the $850.67 displayed balance.

Once you have determined your true balance, now, it’s just a matter of simple math. Just update your balance in your checkbook register by keeping track of each withdrawal and deposit as they occur. This includes debit card transactions as well as checks and automatic payments, as well as your payroll deposits if you have direct deposit.

Once you start logging each transaction, you can cross-reference to what posts to your account. You can either wait until you receive your monthly statement, or you can check daily or every other day, denoting each transaction in your ledger that clears and ensuring the totals match.

By keeping a running total of your transactions, your balance should match the balance on the statement. If the balances don’t match, check your register to see if a transaction has not been processed, if the bank has a record of a transaction that you do not have recorded in your register (then check this transaction to ensure it’s one you recognize or simply forgot to log) or if the amount of one of the transactions differs from what you registered.

If the balances still do not match, check your register and receipts against the record from the bank. Also check for any mathematical mistakes in your register (math mistakes happen to all of us!). If you believe an error has occurred, contact your bank.

Despite checkbooks and checks becoming more obscure in today’s technological landscape, having a handle and knowing just how much money is in your account always will be the most important tool you can have in your financial toolbox and is key to your financial health.

Tracking your transactions keeps you keenly aware of just how much money you have, helps you detect problems and, most importantly, allows you to plan ahead financially.

Financially Fit is your home fitness guide for all things financial, provided by RCB Bank. Find money-building tips, insights and inspiration to help you improve your financial well-being at RCBbank.com/GetFit. Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. Member FDIC.

As inflation continues to rise in the first half of 2022, consumer debt is rising right along with it, according to the Federal Reserve System’s consumer credit report released on Aug. 5.

Consumer debt in the United States is nearly $3.4 trillion, according to the Fed. That is approximately $10,600 of debt for every man, woman and child living in the United States.

Staring at a mountain of debt is daunting. But with proper discipline – and a lot of hard work – you can eliminate your debt.

If you’d like to learn how, read on for these tips on how to greatly reduce and eventually get out of debt.

Know What You Owe and Track Your Spending

You can’t get out of debt if you don’t know where your money is going.

The first step toward taking control of your financial situation is to do a realistic assessment of how much money you take in and how much money you spend, according to Federal Trade Commission.

Start by listing your income from all sources. Then, list your “fixed” expenses — those that are the same each month — like mortgage payments or rent, car payments, and insurance premiums. Next, list the expenses that vary — like groceries, entertainment, and clothing. Writing down all your expenses, even those that seem insignificant, is a helpful way to track your spending patterns, identify necessary expenses, and prioritize the rest.

Change Your Routines

It’s important to account for every penny earned and spent. Most people are shocked at the amount of money spent monthly on fast food lunches, coffee shops and online purchases. Small expenses add up.

By changing your habits – packing a lunch instead of eating out or brewing coffee at home or drinking from the “office pot of coffee,” you can quickly accumulate “extra” money in your budget.

Then you can take those savings and make a debt payment immediately. The instant gratification of seeing balances fall can be extremely motivating.

Tackle Your Debt

Small debt victories likely will make you feel good and motivate you to continue. But you must find a strategy that is right for you, according to the Consumer Financial Protection Bureau. The CFPB even offers a worksheet to help.

Here are the two methods the CFPB recommends. Both strategies have their pros and cons, the CFPB says.

Snowball Method – Tackle one debt at a time.

List all debts in order from smallest to largest.

Pay minimum payment on all debts while throwing as much money as possible to the smallest debt (for example, the money saved by changing your routines.)

After the smallest debt is paid, move on to the next smallest debt until debt free.

Highest Interest Rate Method – Pay a little more than the minimum payment on all debts.

Pay the minimum balance on each debt.

Take extra money and apply it to the debt with the highest interest rate.

Pay off debts in order from highest to lowest interest rates.

Don’t Take on More Debt

You cannot borrow your way out of debt. Low-interest payments and credit cards may indeed be a good deal, but you should work toward paying down what you currently owe before adding any new debt.

It’s important to try to make paying off your debt a top priority, because the way that you manage your credit could determine how much access you have to it in the future. Don’t be afraid to talk to a banker or a financial professional for suggestions on ways to attack your debt situation.

Financially Fit is your home fitness guide for all things financial, provided by RCB Bank. Find money-building tips, insights and inspiration to help you improve your financial well-being at RCBbank.com/GetFit. Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. Member FDIC.

Recently there has been a rise in email fraud where a scammer poses as a major retailer, luring unsuspecting people with claims that an expensive purchase was made by them. The email will give a number to call if the email recipient doesn’t recognize or wants to dispute the purchase.

This is a common phishing scam. The scammer simply wants you to call the number, and that’s when they’ll try to get information out of you.

Once the scammers get you on the phone, they’ll sound official. They may ask who you bank with. They’ll ask you for your account number and passwords.

Don’t fall for it. Do not give any personal information once they ask for it, no matter how official they sound. If they ask for access to your computer or mobile device, hang up!

There will be several red flags to look for if you receive such an email:

The email address won’t have the business’s name or domain.

There will be spelling and grammar errors in the email.

When hovering over links, the displayed website doesn’t direct to the business.

It may look like a reply to an email you never sent.

The business logos and images are blurry.

Don’t just call a number you receive in an email without researching the phone number first. Review your accounts to see if any unauthorized charges were made. If you don’t see any charges that are mentioned in the email, it’s very likely a scam.

If you believe you’ve been scammed, call your bank’s fraud department. You also can report fraud to the FTC at https://reportfraud.ftc.gov/.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

As the world continues to move more toward digital transactions, more and more businesses and organizations utilize digital payment methods. Digital payments have boomed since the start of the COVID-19 pandemic because of their flexibility and ease of use.

But as more digital payment processing companies begin to emerge, scammers adapt. A new scam that has been on the rise is a micro-deposit scam.

Micro-deposits are small amounts of money – generally under $1 – that are transferred from one account to another. They typically come in pairs and in separate amounts, usually coming within three days of linking accounts. The purpose of micro-deposits is to verify if the account on the receiving end is the account that is intended to be linked to the depositing account.

So far, everything described is common when linking accounts.

But how micro-deposit scammers operate is by linking online accounts with strings of random numbers, just hoping to get a valid bank account. When a deposit is verified from a bank account, the fraudsters will use information about the account holder to withdraw funds from their account.

The best way to combat this type of fraud is to monitor your account regularly. If you notice a micro-deposit, DO NOT verify it if you didn’t initiate it and DO NOT click on any links that are embedded in a verification request message or download any attachments in a verification email.

If you’ve been the victim or a target of a micro-deposit scam, contact your bank to ensure it won’t happen again. And then contact the Federal Trade Commission at https://reportfraud.ftc.gov/.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Spring traditionally is a time of regrowth, new life and budding. You may get the itch to deep clean and organize your house.

And while you’re at it, you should consider a “spring cleaning” of your mortgage as well. These tips could lead to saving money, so take the time to look to see if any of these situations apply to you.

Private Mortgage Insurance

Private Mortgage Insurance, known as PMI, is required on some loans. If you started your loan with PMI, it will fall off once you reached the date when the principal balance of your mortgage is scheduled to fall to 78 percent of the original value of your home. This date should have been given to you in writing on a PMI disclosure form when you received your mortgage. If you can’t find the disclosure form, contact your servicer. Also, if your home has increased in value since you purchased it, your Loan to Value (LTV) ratio may be at a point to discontinue your PMI early. You can request this from your lender and they would determine with an updated evaluation of your home with an appraisal. Discontinuing your PMI can free up some extra money each month if this applies to you.

Insurance

Check to see if your homeowner’s insurance policy has risen, and shop around for a lower rate. Getting a quote costs no money. Are you bundling your home and auto policies? Most insurance carriers offer a discount for bundling policies. It’s a good idea to get quotes to see if there’s savings of which you weren’t aware. Also check to see if your agent might have you over-insured. Lowering your policy to what you only need vs. more than you need could lower your cost as well.

Tax refund

If you receive a tax refund, consider using it as an additional payment toward the principal of your mortgage. Making one additional monthly payment a year can shave up to four years off your mortgage!

Refinancing

Now is a good time to think about refinancing your home. If you’ve owned your home for awhile and don’t plan on moving anytime soon, refinancing likely will save you a significant amount of money. In some cases, refinancing to a 15-year mortgage will make more sense.

Lenders at RCB Bank are happy to help answer questions even if you are not a customer. Give us a call or visit our online Mortgage Center.

Opinions expressed above are the personal opinions of RCB Bank personnel and meant for generic illustration purposes only. With approved credit. For specific questions regarding your personal lending needs, please call RCB Bank at 855-BANK-RCB. Some restrictions apply. RCB Bank is an Equal Housing Lender and member FDIC. RCB Bank NMLS #798151.

As tax season kicks into high gear, scammers are looking to take advantage. Scammers will make aggressive phone calls posing as IRS agents, hoping to steal money or information from victims.

Scammers will demand immediate payment for tax bills, regardless of whether you owe taxes or not. And if you give the scammers personal information, that can lead to identity theft, which in turn could lead to the scammer filing tax returns in your name and stealing your tax refund – in addition to other negative financial effects.

“With filing season underway, this is a prime period for identity thieves to hit people with realistic-looking emails and texts about their tax returns and refunds,” IRS Commissioner Chuck Rettig said. “Watching out for these common scams can keep people from becoming victims of identity theft and protect their sensitive personal information that can be used to file tax returns and steal refunds.”

Be on high alert if you receive a call, text or email asking to disclose your personal information. Don’t click on any links if you receive an email, and don’t respond to any texts.

If you receive one of these calls, hang up immediately. You can report any email you receive and report the phone number from which you received a suspicious call or text by emailing the IRS at [email protected].

To ensure you stay safe this tax season, remember that the IRS will NEVER:

Demand immediate payment using a specific method, such as a prepaid debit card, gift card or wire transfer.

Threaten to immediately bring in law enforcement groups and arrest you for not paying.

Demand that your taxes be paid without giving you an opportunity to question or appeal the amount owed.

Call unexpectedly about a tax refund.

Initiate taxpayer communications through email – ever.

Stay alert and safe this tax season, and remember the deadline to file your taxes is Monday, April 18, 2022.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

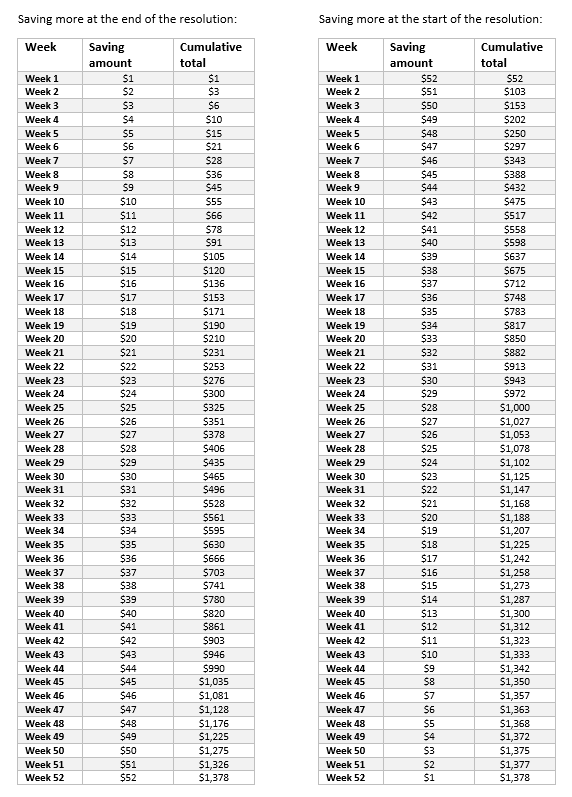

New Year’s resolutions help keep people motivated to stick to their new-year goals. And if you’re looking to kick-start your savings this year, try the 52-week savings resolution.

Just think, by the end of the year, you could have nearly $1,500 stashed away.

What you do with the money accrued from this savings is up to you. It could be set aside and used strictly for emergencies. It could be used for your Christmas shopping. It could be used to pay for a well-earned vacation.

Or you could choose to keep it in your savings account and add to it with the same challenge next year.

The basis of the challenge is simple: Every week, you add money to your savings account. In Week 1, you save $1. In Week 2, you save $2, and so on, all the way to Week 52, where you will save $52.

At the end of the year using this method, you’ll have saved $1,378.

With this method, the brunt of the savings comes toward the end of the year. And for many, that could be a hefty amount of money to sock away during the holiday season.

If that seems like it’s too daunting of a task, you can reverse the order of savings: i.e. save $52 in Week 1, $51 in Week 2, $50 in Week 3, and so on, all the way to Week 52, where you will save $1.

Here is an example of how the plans will look:

Even if there are some weeks where you can’t meet that week’s savings goal, save what you can that week. There may be some weeks where you can catch up later in the year. Or there may be some weeks earlier in the year where you can save more.

Whatever you do, don’t give up. Staying motivated is the key to sticking with your resolutions, and watching your money grow weekly can help keep you motivated. If you’re ready to get started, click below for more information.

Financially Fit is your home fitness guide for all things financial, provided by RCB Bank. Find money-building tips, insights and inspiration to help you improve your financial well-being at RCBbank.com/GetFit. Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Timing is everything, and that is especially true when purchasing a house. Whether you’re waiting for the right home or applying for a mortgage, there are many time-sensitive processes to follow to ensure you can get the home and the financing you want.

It may seem like there’s a lot of hurry up and wait going on. But because it is likely the biggest purchase you’ll make in your life, there’s a good reason for the wait.

For traditional mortgages, the most noticeable is the three business-day waiting period between receiving your closing disclosure and the consummation date (often known as your closing day). This three business-day rule was introduced in October of 2015, and it applies to both original mortgages and refinancing.

When your three business-day waiting period starts is determined by your consummation day. This three business-day rule may include Saturdays, but it does not count Sundays or holidays.

For instance, if you want to sign on a Friday and a holiday falls on a Thursday, you must receive your closing disclosure on Monday. Because of this, the three-day period is NOT measured by hours.

You can sign the closing disclosure any time before you sign your final documents on your consummation day.

This waiting period gives you time to review all the documents to ensure that the terms you’re agreeing to match the terms outlined at the beginning of the mortgage process when you received your loan estimate (which lenders are required to disclose no later than three days after receiving your completed application).

The closing disclosure will show you the final terms of your mortgage, including your purchase price, interest rate, APR, closing costs, monthly payment, and more. Between the closing disclosure and consummation, if the APR, loan product type or prepayment penalty changes, that would require a revised closing disclosure, which in turn would require a new consummation date. Other changes to terms and costs outside of these (like title fees and insurance), will warrant a corrected closing disclosure, but will not require a new three business-day waiting period.

Basically, the closing disclosure is designed to protect you from bait-and-switch tactics if a lender promised you one set of terms but then presents worse terms just prior to the consummation day.

Opinions expressed above are the personal opinions of RCB Bank personnel and meant for generic illustration purposes only. With approved credit. For specific questions regarding your personal lending needs, please call RCB Bank at 855-BANK-RCB. Some restrictions apply. RCB Bank is an Equal Housing Lender and member FDIC. RCB Bank NMLS #798151.

‘Tis the season for scams.

This Christmas season, be on the lookout for scams and fraud. The Christmas season is the busiest shopping part of the year, and scammers are in full swing waiting to take advantage.

As many retailers begin their Christmas sale specials, scammers are ready with fraudulent websites and social media campaigns, impersonating those retailers. The scammers are hoping to entice you to spend money for products you’ll never receive.

Add in projected shipping delays and supply chain issues, and this Christmas season scammers are projected to be rife. Scammers preying on those will offer products that aren’t available or products that may not be quite what they seem.

Scammers generally won’t have any new tricks during the holiday season, but they will try different spins on scams that have worked in the past. During the Christmas season, scammers thrive as many tend to be more generous and in a giving spirit.

Here are some seasonal scams of which to be aware:

Charity scams

One-third of all charitable giving is done in December, fundraising software company Network for Good reports. That means more sham charities exploiting Americans’ goodwill via fake websites and pushy telemarketers.

Delivery scams

As holiday packages crisscross the country, scammers send out phishing emails disguised as UPS, FedEx or U.S. Postal Service notifications of incoming or missed deliveries. Links lead to phony sign-in pages asking for personal information, or to sites infested with malware.

Travel scams

Nearly 50% of U.S. adults plan to travel during the holidays in 2021, a SurveyMonkey poll found. Spoof booking sites and email offers proliferate, with travel deals that look too good to be true and probably are.

Letter from Santa scams

A custom letter from Ol’ Saint Nick makes a holiday treat for the little ones on your list, and many legitimate businesses offer them. But so do many scammers looking to scavenge personal information about you or, worse, your kids or grandkids, who may not learn until many years later that their identity was stolen and their credit compromised.

Gift card scams

When purchasing gift cards, make sure to purchase from counter attendants or from customer service. Thieves will copy the codes on cards and call after the holidays (when they know they will be activated) and use them before the intended recipient gets a chance to. Grabbing a card from an unattended sales rack increases the chances of having this happen to you.

Being aware of the types of scams that scammers use can help keep you — and your money — safe this Christmas season.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

The holidays are a time when it’s tempting – and easy – to toss your budget out the window and splurge on your friends and family.

After all, it’s the season of giving. And often, giving the perfect gift is just as fun as receiving a gift.

However, with proper planning, you can stay on budget while spreading Christmas joy and avoiding the stresses that come with searching for that perfect present.

There’s no magic secret to a holiday budget. You’ll have to put the pen to the paper and figure out ahead of time how much you can afford to spend. Then you have to stick to it.

In other words, make a list and check it twice.

Having a budgeted list and sticking to it will help you navigate all the expenses that come with the holidays.

Make a list of everyone you need to buy for and then a price range for each person with gift ideas. If you do this, it will come in handy later.

Let’s say you find a great deal on a gift for one person on your list and it comes in $25 under budget. That can help you later if a gift you found for another person is $20 over budget – you can still purchase that gift, because you were under budget on the first person.

One final tip is to start thinking about next year. Save your receipts. They can come in handy next Christmas when making your budget. You’ll know who all you shopped for and how much you spent on them.

Also, when planning for next year’s Christmas budget, talk to your bank and see if they have options that will help you save throughout the year. They’ll most likely be happy to set up a separate account that you can deposit money into every payday. Then you’ll automatically have your money ready to go!

Make it a challenge to see if you can come in under budget. If that happens, you can reward someone who wasn’t on your list – yourself!

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, member FDIC.

With the recent news of Social Security benefits increasing by nearly 6% in 2022, now is the time to be on the lookout for Social Security scammers.

Those who receive Social Security benefits don’t have to do anything to receive the increase. The increases will happen automatically.

However, scammers will try to take advantage of those who are unaware that their increase will happen automatically.

These tips from the Social Security Administration (SSA) show you what to look for and how to recognize a Social Security scammer:

Social Security scammers may:

Threaten arrest or legal action against you unless you pay a fine.

Promise to increase your benefits or resolve identity theft if you pay a fee.

Demand payment with retail gift cards, wire transfers, internet currency or by mailing cash.

Pretend they are from Social Security or another government agency. Caller ID, texts or documents sent by email may look official but they are not.

DO NOT BELIEVE THEM!

If you owe money to Social Security, the agency will mail you a letter with payment options and appeal rights. Social Security does not suspend Social Security numbers or demand secrecy from you, ever.

How you can help:

If you receive a questionable call, hang up and report it at ssa.gov.

Do not return unknown calls, email, or texts.

Ask someone you trust for advice before making any large purchase or financial decision.

Do not be embarrassed to report if you shared personal information or suffered a financial loss.

If you think you’ve been a victim of a scammer, call the SSA fraud hotline at 1-800-269-0271.

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Source:

https://www.ssa.gov/scam/

Spoof websites can lure unsuspecting people into giving away their information without knowing that they’re doing it. A spoof website will try to make itself look almost exactly like the website it is trying to spoof, hoping a person will enter their personal information or username and password.

Once a scammer’s fake, but legitimate-looking website gets indexed by search engines, it will appear in search results based on the search words you type.

Even if you are a seasoned internet user, it is easy to fall prey to the sophisticated techniques that are used in website spoofing. With the wool pulled over your eyes, you could inadvertently give phishers extremely damaging information. The best way to handle spoofed websites is by exercising caution at all times.

Finding your way onto a spoofed website usually happens by using vague or incorrect search engine terms. It also can happen if you type a web address too quickly and accidentally transpose two letters or misspell the web address.

How to spot spoof websites

There are several ways to spot a fake website:

Misspellings and grammar mistakes: While most fraudulent websites try to make it look as close to the actual website they’re trying to spoof as possible, misspellings or improper capitalization of words sometimes creep in. Also look for missing periods or commas

Take a close look at the URL: If the URL isn’t what you expect it to be, it’s probably a spoof website. Close that website as soon as possible.

Blurry logos or images: Because spoof websites don’t have access to original company logos and images, the ones they’ll use are lower resolution and likely will appear to be blurry on the spoof website.

If you see any of these red flags, don’t click on any links.

How to prevent visiting a spoof website

If it is a website you visit often, such as your bank website, bookmarking the website and accessing it directly via the bookmark will prevent you from accidentally typing in the website address incorrectly.

Also, be extra careful when using a search engine. Ensure the words are spelled correctly.

Before clicking on a link, hover over it and read the true website address at the bottom left of the browser. If it isn’t familiar, don’t click on the link.

By taking your time and being careful, you should be able to avoid most problems.

What to do if you suspect a spoof website

If you happen across a spoofed website, you can report the fake website to the federal government here:

Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

Starting a savings plan for emergencies may seem like a daunting task. Your goal may seem unreachable or impossible, especially if you’re living paycheck to paycheck.

According to a May 2021 survey, not saving enough for emergencies is Americans’ biggest financial regret.

But why is an emergency savings plan important? Because while you can’t control when something unexpected happens to you, you can control being prepared for the unexpected.

Imagine your air conditioner going out in the July heat on the hottest day of the year. Or, your car breaking down. Unforeseen circumstances can cause problems that can then snowball, if not addressed as soon as possible.

An emergency savings plan creates a financial buffer which helps in times of need and can stave off debt. An emergency savings fund can keep you from needing to take out a payday loan or using high-cost credit cards to cover the cost of the emergency.

According to a July 2021 survey, more than half of Americans have less than three months’ worth of expenses saved in an emergency fund – and 25% have no emergency fund at all – which is up from 21 percent in 2020.

Three months’ worth of savings won’t happen overnight.

So how do you start saving?

If money is tight, start small, with a goal of saving $100. Then $500. Then $1,000. Work your way up to six months’ worth of expenses. It’s not about how much money you make — it is how you manage your money that matters.

Once you have it established, resist the temptation to dip into it.

Have the money direct deposited from your paycheck into a designated emergency fund account – not your checking account – so it’s automatic.

Financially Fit is your home fitness guide for all things financial, provided by RCB Bank. Find money-building tips, insights and inspiration to help you improve your financial well-being at RCBbank.com/GetFit. Opinions expressed above are the personal opinions of the author and meant for generic illustration purposes only. RCB Bank, Member FDIC.

What is auto refinancing?

Auto refinancing is when you replace your current automobile loan with a new loan that has better or different terms. The new loan pays off your original loan and you open a new loan with new paperwork, a new loan rate and new terms and conditions.

When to Refinance Your Car

There are many reasons why someone might need or want to refinance their car:

• Interest rates have gone down since you took out your original loan. If interest rates have dropped, it is worth talking to a lender and seeing what your potential savings could be over the life of the loan.

• You didn’t get the best deal possible when you purchased the car and would like a more favorable loan now. Car dealerships may not offer the best rates possible. If you took out your loan with a dealer and did not negotiate the interest rate, a refinance could save you a lot of money over the life of the loan.

• Your personal finances have changed and you would like a lower monthly payment. While refinancing can reduce your monthly payments, it often means taking a longer loan payoff period. Your car will also depreciate during that time and you may pay more in interest over the life of the loan. Term restrictions may also apply depending on the year of the vehicle.

• Your credit has improved since you received your original loan. If you previously had bad credit or no credit, checking to see if you can get a better deal a few years down the road is a good idea. You may receive better offers and save money over the life of the loan with a lower interest rate.

How to Refinance Your Car

Before you decide to refinance, talk to a few lenders to see what rates they offer and whether it will save you money over the life of the loan. Find out if there is a prepayment penalty, or fee for paying off your other loan early, and what others fees you may be responsible for when you refinance. You will also want to make sure your car’s value is more than the loan amount left, or it could be hard to get a new loan. Some lenders may have restrictions about the age of the car they will refinance.

Once you have determined if refinancing is a good option, prepare your documentation. You will likely need a number of documents on hand to apply for a new loan.

• Proof of income

• Evidence of auto insurance.

• Information on your current loan.

• Information about the car, including the make, model, mileage, year and vehicle identification number, or VIN.

• Your driver’s license.

After you have gathered your documentation, shop around. Look for loan promotions in your area and get prequalified with a few different lenders. Some lenders also offer a discount if you use an automatic payment option, so don’t forget to ask.

GAP Insurance

GAP, also known as Guaranteed Asset Protection, provides the consumer with protection in the event of a total loss of the covered car due to vehicle theft or an accident. If a total loss occurs, you file a claim and GAP will pay off the residual loan balance that the primary claim fails to pay. Given the ever-increasing costs of a complete vehicle restoration after an accident, GAP protection may be needed more now than ever before.

When to Get Car GAP Insurance

As a general rule, if you have less than 20% equity in on the car when you open the loan, GAP coverage should be considered. Conversely, if you enter the loan with more than 20% equity in the car, GAP coverage becomes less beneficial and effective. Also, the longer the loan period, the more helpful GAP coverage becomes.